Formats of Financial Statements for Non-Corporate Entities: A Practical Guide

Stay ahead of the curve with our latest guide on the ICAI’s Guidance Note for Non-Corporate Entities. This blog unpacks the new financial statement formats, explains who needs to comply, and offers practical steps for smooth implementation. Discover common pitfalls, a handy disclosure checklist, and expert tips to ensure your financial statements are both compliant and insightful. Perfect for proprietors, partners, and managers looking to navigate these changes with confidence.

ACCOUNTING

7/6/20253 min read

Formats of Financial Statements for Non-Corporate Entities: A Practical Guide

Are you a proprietor, a partner in a firm, or managing a trust or society? If so, there’s important news you can’t afford to miss. The ICAI has just rolled out a new Guidance Note on Financial Statements of Non-Corporate Entities, bringing a fresh wave of clarity and uniformity to how financials are prepared and presented. Whether you’re a seasoned professional or just getting started, these changes will shape the way your entity reports its financial health from this year onward.

What does this mean for your business? Who needs to follow these formats, and how can you ensure a smooth transition without missing any crucial details? In this blog, we break down everything you need to know—right from the date of applicability, practical steps for management, common pitfalls, and a handy last-minute disclosure checklist. Read on to make sure your financial statements are not just compliant, but also a true reflection of your entity’s performance and credibility.

a. Date of Applicability

The Guidance Note is applicable for financial statements covering periods beginning on or after 1st April 2024. This means that for most entities, the financial year 2024-25 will be the first to follow these new formats. Early preparation and understanding will help avoid last-minute challenges.

b. Entities Required to Follow These Formats

The formats prescribed in the Guidance Note are mandatory for all non-corporate entities, including:

Sole proprietorships

Partnership firms

Hindu Undivided Families (HUFs)

Trusts

Societies

Associations of Persons (AOPs) and Bodies of Individuals (BOIs)

It’s important to note that Limited Liability Partnerships (LLPs) are excluded as they fall under corporate entities and follow a different set of reporting standards. Entities governed by specific laws with their own prescribed formats should continue with those but may refer to this Guidance Note for additional disclosures.

c. How Management Should Apply These Formats: Approach and Methodology

To ensure seamless compliance, management should adopt a structured approach:

Familiarize with the Format: The new formats are aligned closely with Schedule III of the Companies Act but tailored for non-corporate entities. Understanding the layout and requirements is the first step.

Classify Your Entity: Entities are categorized into Levels I to IV based on turnover, borrowings, and regulatory oversight. Level I entities follow the full format, while Levels II-IV enjoy certain relaxations.

Revise Accounting Policies: Update and customize accounting policies to reflect your entity’s nature and operations accurately. Avoid generic policies that don’t address specific circumstances.

Prepare Comparative Statements: Present figures for both the current and previous financial years side by side for better clarity and analysis.

Ensure Accurate Classification: Properly segregate assets and liabilities into current and non-current categories, and distinguish between financial and non-financial items.

Develop Detailed Notes to Accounts: Prepare comprehensive notes covering all mandatory disclosures, accounting estimates, and judgments to provide transparency.

This methodical approach not only helps in compliance but also enhances the usefulness of financial statements for stakeholders.

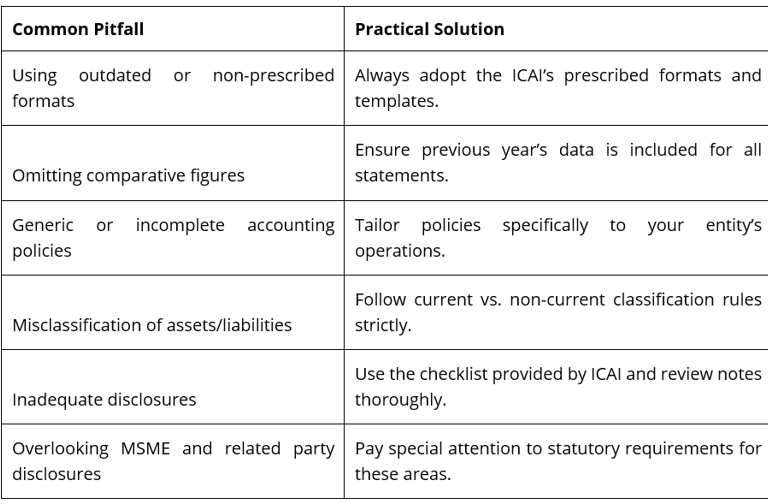

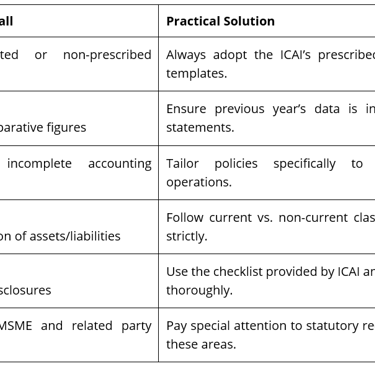

d. Key Areas Prone to Mistakes and How to Overcome Them

Regular internal audits and cross-checks can help identify and rectify these errors early.

e. Handy List of Disclosures for Last-Minute Review

Before finalizing your financial statements, ensure the following disclosures are complete and accurate:

Updated accounting policies specific to your entity

Details of capital contributions, drawings, and partner current accounts

Breakdowns and ageing schedules of receivables and payables, including MSME disclosures

Contingent liabilities and commitments

Methods of revenue recognition and depreciation

Information on related party transactions

Key estimates and judgments made during preparation

Details of borrowings, guarantees, and securities

Segment information (if applicable)

Events after the reporting period

Comparative figures for all financial statements

Any additional regulatory disclosures relevant to your entity’s category or sector

Conclusion

The ICAI’s Guidance Note on Financial Statements of Non-Corporate Entities is a welcome development that promotes transparency, consistency, and reliability in financial reporting. By understanding the applicability, following a clear methodology, and paying careful attention to common pitfalls and disclosure requirements, management can ensure their financial statements not only comply with regulatory standards but also provide meaningful insights to stakeholders.

Early adoption and diligent application of these formats will help your entity build credibility and foster trust among investors, lenders, and regulators alike.

If you need further assistance or customized support in implementing these formats, consulting with us would make the transition smoother and more efficient.

Get In Touch

Delhi

HO: S-433, Greater Kailash Part - I,

New Delhi - 110048

Branch office : C - 6/162, Yamuna Vihar,

New Delhi - 110053

Meerut

D-181/14, 2nd Floor, Saraswati Lok, Madhavpuram, Meerut, Uttar Pradesh

+91- 9205689968

office@canmn.in

Submit Your Query

© NMN & Associates 2025. All rights reserved.

Working Hours

Monday to Saturday

9:30 AM to 6:30 PM